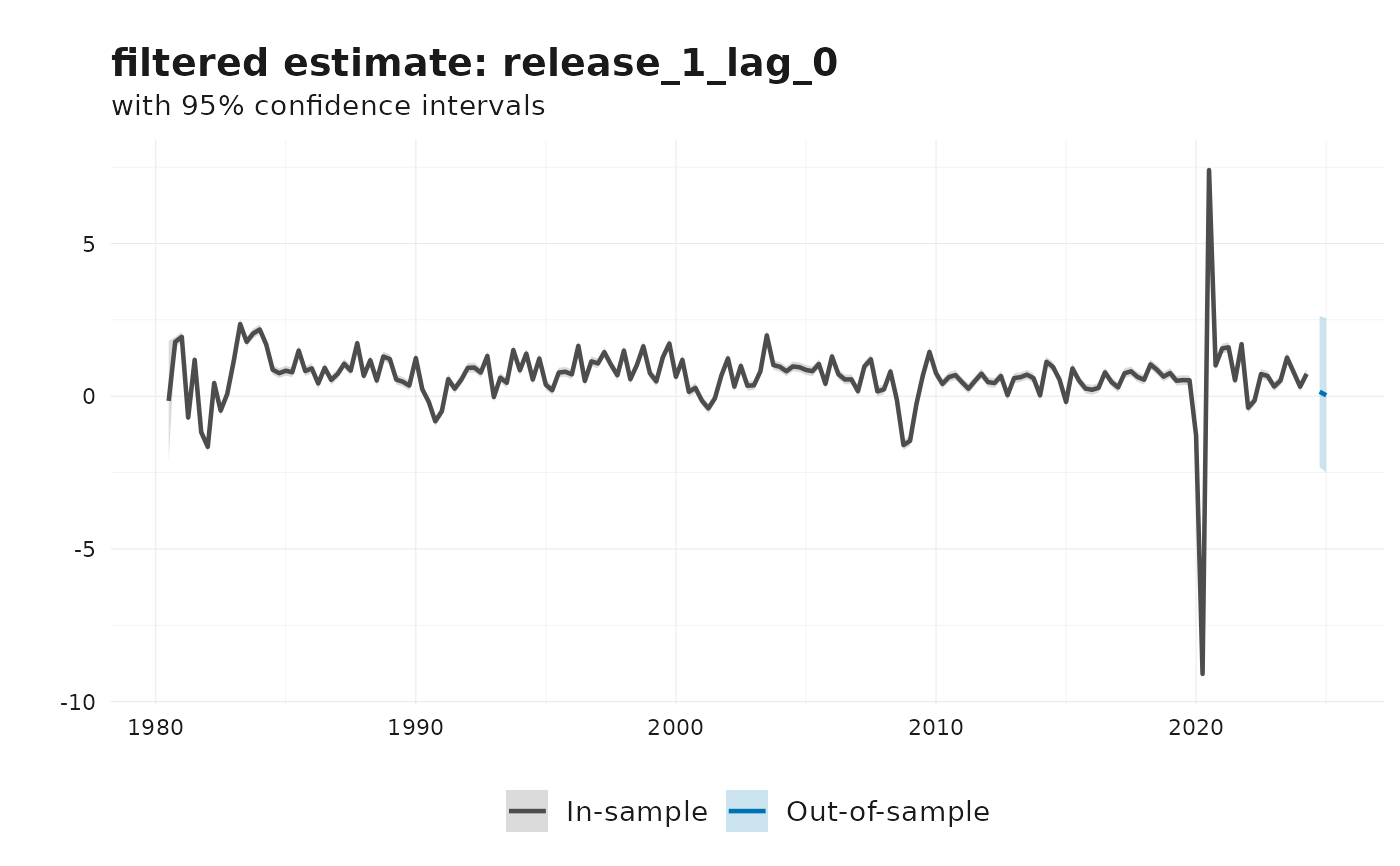

Plot filtered or smoothed estimates for a selected state from a fitted

kk_model.

Usage

# S3 method for class 'kk_model'

plot(x, state = NULL, type = "filtered", ...)Details

This method requires x$states to be available. If the model was

fitted with solver_options$return_states = FALSE, plotting is not

possible.

See also

Other revision nowcasting:

jvn_nowcast(),

kk_nowcast(),

plot.jvn_model(),

print.jvn_model(),

print.kk_model(),

summary.jvn_model(),

summary.kk_model()

Examples

df <- get_nth_release(

tsbox::ts_span(

tsbox::ts_pc(

dplyr::filter(reviser::gdp, id == "US")

),

start = "1980-01-01"

),

n = 0:1

)

df <- dplyr::select(df, -c("id", "pub_date"))

df <- na.omit(df)

e <- 1 # Number of efficient release

h <- 2 # Forecast horizon

result <- kk_nowcast(df, e, h = h, model = "Kishor-Koenig")

plot(result)