Nowcasting revisions using the generalized Kishor-Koenig family

Source:vignettes/nowcasting-revisions-kk.Rmd

nowcasting-revisions-kk.RmdThis vignette describes the generalized Kishor-Koenig (KK) revision

model and its nested variants as implemented in

reviser::kk_nowcast(). The exposition uses the same

Durbin-Koopman state-space notation that appears throughout the package

documentation: observation matrices are denoted by

,

transition matrices by

,

shock-loading matrices by

,

and disturbance covariance matrices by

and

(Durbin and Koopman

2012).

The motivation is straightforward. Early releases of macroeconomic series are often revised several times before they settle near a stable value. Rather than ignoring that revision process, the KK family models the vector of releases directly and uses the Kalman filter to infer the latent efficient estimate.

Revision system

Suppose that an efficient estimate becomes available after revisions. Let denote the -th release for reference period , where . Following Strohsal and Wolf (2020), stack the efficient estimates and the observed real-time releases as

The generalized KK model is

The companion-form transition matrix is

and the gain matrix is

Intuitively, governs the dynamics of the efficient estimate, while controls how quickly incoming releases absorb new information. The covariance matrices and describe uncertainty in the latent efficient estimate and the published releases, respectively.

Nested models

The generalized KK setup nests two useful special cases.

- The Classical measurement-error model is obtained by setting . In that case, published data are noisy measurements of the latent efficient estimate, with no revision persistence beyond the state dynamics.

- The Howrey model (Howrey 1978) allows revision persistence but restricts the gain matrix by imposing for and .

The model argument in kk_nowcast() selects

among these specifications: "KK", "Howrey",

and "Classical".

Durbin-Koopman state-space form

To run filtering and smoothing, reviser casts the KK

system into the standard time-invariant state-space form

Define the augmented state as

With this choice of state vector, the implementation in

kk_to_ss() uses

The observation disturbance is set to zero, so . All uncertainty is collected in the state disturbance covariance matrix

This is exactly the Durbin-Koopman representation used internally by

reviser: the Kalman filter and smoother operate on

,

while the KK-specific parameters

remain the economically interpretable layer.

Estimation in reviser

kk_nowcast() supports three estimators.

-

method = "SUR"estimates the original revision equations jointly by seemingly unrelated regression usingsystemfit::nlsystemfit(). -

method = "OLS"estimates the equations one by one. This is fast, but the cross-equation restrictions are not fully efficient. -

method = "MLE"estimates the state-space model by maximum likelihood using the Kalman filter.

For applied work, the MLE route is usually the most flexible because it supports information criteria, Hessian- or QML-based standard errors, and filtered or smoothed states directly from the state-space model.

Example: Euro Area GDP revisions

We illustrate the workflow with Euro Area GDP growth from

reviser::gdp. We first identify an efficient release among

the first 15 vintages, then estimate the full KK model.

library(reviser)

library(dplyr)

library(tidyr)

library(tsbox)

gdp <- reviser::gdp |>

tsbox::ts_pc() |>

dplyr::filter(

id == "EA",

time >= min(pub_date),

time <= as.Date("2020-01-01")

) |>

tidyr::drop_na()

df <- get_nth_release(gdp, n = 0:14)

final_release <- get_nth_release(gdp, n = 15)

efficient_release <- load_or_build_vignette_result(

"nowcasting-revisions-kk-efficient-release.rds",

function() get_first_efficient_release(df, final_release)

)

summary(efficient_release)

#> Efficient release: 2

#>

#> Model summary:

#>

#> Call:

#> stats::lm(formula = formula, data = df_wide)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.34873 -0.08185 -0.00706 0.10475 0.31533

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 0.03276 0.01775 1.846 0.0692 .

#> release_2 1.01446 0.02440 41.577 <2e-16 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Residual standard error: 0.1428 on 68 degrees of freedom

#> Multiple R-squared: 0.9622, Adjusted R-squared: 0.9616

#> F-statistic: 1729 on 1 and 68 DF, p-value: < 2.2e-16

#>

#>

#> Test summary:

#>

#> Linear hypothesis test:

#> (Intercept) = 0

#> release_2 = 1

#>

#> Model 1: restricted model

#> Model 2: final ~ release_2

#>

#> Note: Coefficient covariance matrix supplied.

#>

#> Res.Df Df F Pr(>F)

#> 1 70

#> 2 68 2 2.743 0.07151 .

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

data_kk <- efficient_release$data

e <- efficient_release$eThe selected value of e tells us how many revision

rounds are needed before a release is statistically close to the final

benchmark.

fit_kk <- load_or_build_vignette_result(

"nowcasting-revisions-kk-fit.rds",

function() {

kk_nowcast(

df = data_kk,

e = e,

model = "KK",

method = "MLE",

solver_options = list(

method = "L-BFGS-B",

maxiter = 100,

se_method = "hessian"

)

)

}

)

summary(fit_kk)

#>

#> === Kishor-Koenig Model ===

#>

#> Convergence: Success

#> Log-likelihood: 125.7

#> AIC: -231.41

#> BIC: -198.23

#>

#> Parameter Estimates:

#> Parameter Estimate Std.Error

#> F0 0.633 0.131

#> G0_0 0.950 0.031

#> G0_1 -0.037 0.152

#> G0_2 -0.181 0.220

#> G1_0 -0.009 0.011

#> G1_1 0.594 0.061

#> G1_2 0.194 0.092

#> v0 0.380 0.068

#> eps0 0.008 0.001

#> eps1 0.001 0.000The parameter table reports the estimated transition coefficient , the gain-matrix elements , and the state and observation variances.

fit_kk$params

#> Parameter Estimate Std.Error

#> 1 F0 0.632965335 0.1313813639

#> 2 G0_0 0.950076539 0.0308315303

#> 3 G0_1 -0.036660310 0.1517629398

#> 4 G0_2 -0.180790257 0.2201177887

#> 5 G1_0 -0.008913846 0.0109883743

#> 6 G1_1 0.594486360 0.0612313441

#> 7 G1_2 0.194005812 0.0915497686

#> 8 v0 0.379874788 0.0683792923

#> 9 eps0 0.007785910 0.0014196296

#> 10 eps1 0.001397112 0.0002435075The states element contains filtered and smoothed

estimates of the latent state vector in tidy format.

fit_kk$states |>

dplyr::filter(filter == "smoothed") |>

dplyr::slice_tail(n = 8)

#> # A tibble: 8 × 7

#> time state estimate lower upper filter sample

#> <date> <chr> <dbl> <dbl> <dbl> <chr> <chr>

#> 1 2018-04-01 release_2_lag_2 0.654 0.652 0.656 smoothed in_sample

#> 2 2018-07-01 release_2_lag_2 0.370 0.368 0.372 smoothed in_sample

#> 3 2018-10-01 release_2_lag_2 0.414 0.412 0.416 smoothed in_sample

#> 4 2019-01-01 release_2_lag_2 0.136 0.134 0.138 smoothed in_sample

#> 5 2019-04-01 release_2_lag_2 0.307 0.305 0.309 smoothed in_sample

#> 6 2019-07-01 release_2_lag_2 0.441 0.439 0.443 smoothed in_sample

#> 7 2019-10-01 release_2_lag_2 0.147 0.146 0.149 smoothed in_sample

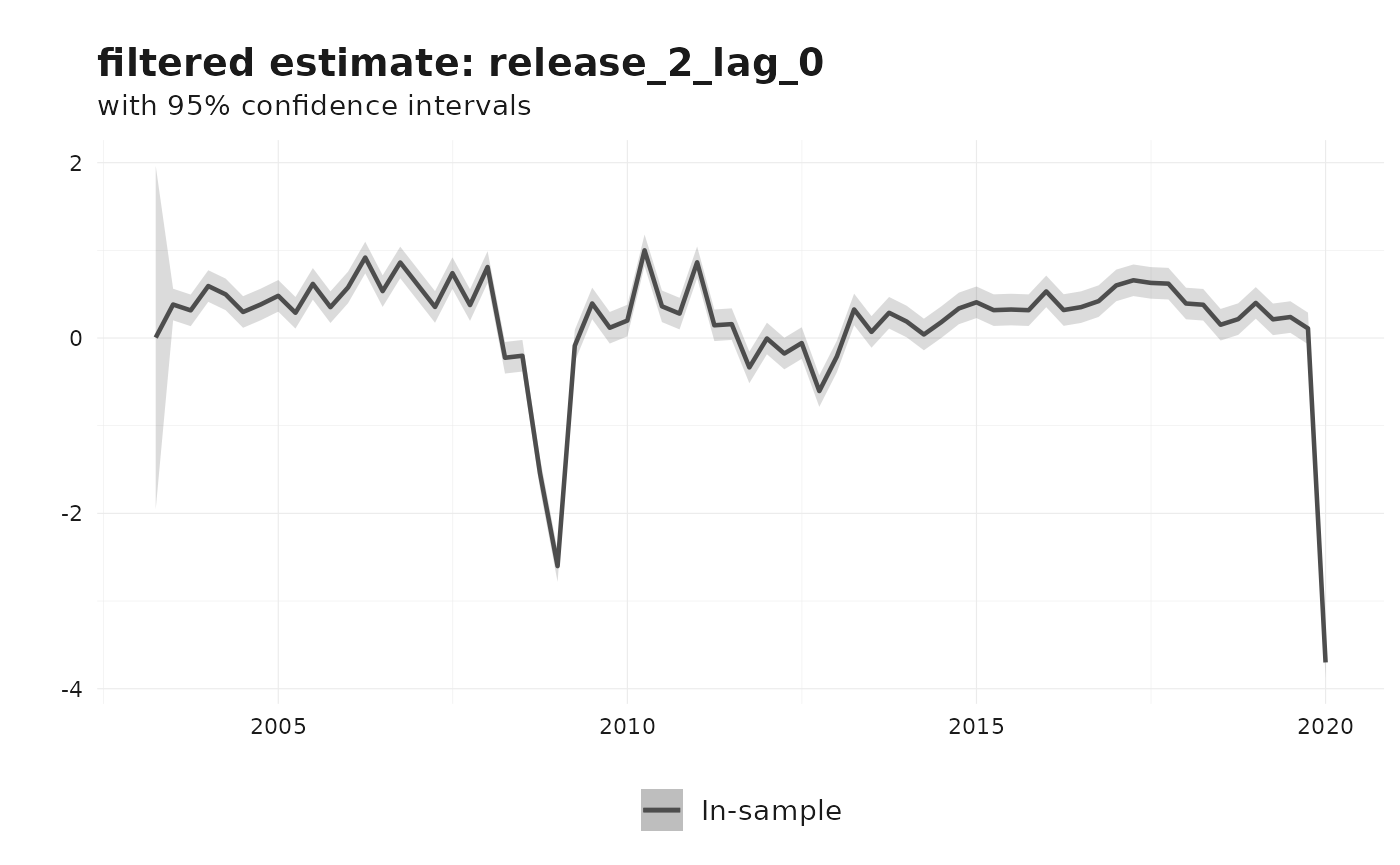

#> 8 2020-01-01 release_2_lag_2 0.299 0.297 0.301 smoothed in_sampleThe default plot method shows the filtered estimate of the efficient release and its confidence interval.

plot(fit_kk)

Other KK-family specifications

The same data can be estimated under the nested Howrey and Classical restrictions.

fit_howrey <- kk_nowcast(

df = data_kk,

e = e,

model = "Howrey",

method = "MLE"

)

fit_classical <- kk_nowcast(

df = data_kk,

e = e,

model = "Classical",

method = "MLE"

)Those alternatives are useful when the unrestricted gain matrix of the full KK model is too parameter rich for the available sample.